Over the past decade, instant payment systems have established themselves as essential infrastructure for modernizing the financial sector in emerging economies. Colombia has not been immune to this trend: the way Colombians make payments and transfers has shifted significantly.

The growth of digital wallets, electronic transfers, and QR codes has favored the digitization of payments and access to financial services. However, these advances have coexisted with a lack of interoperability among multiple service providers, which has limited the adoption of electronic payments and contributed to a high use of cash (the instrument preferred by 78.6% of adults in 20231).

As detailed in the recent publication, Bre-B, Colombia’s interoperated instant payments system, whose design began in 2022 and which came into operation on October 6, 2025, emerged in response to these challenges. It is a public policy guided by Banco de la República (the Central Bank of Colombia) in collaboration with the industry, based on existing instant payment solutions, to encourage competition and facilitate adoption through a unified user experience.

The design of Bre-B

In 2022, Banco de la República convened the Payment Systems Forum, bringing together financial institutions, cooperatives, fintechs, trade associations, and international experts. Its conclusions highlighted the need for an interoperable solution for instant payments, beyond existing industry innovations. This context gave rise to Article 104 of the Development Plan (Law 2294 of 2023), which granted the Board of Directors of Banco de la República (BDBR) the power to regulate the interoperability of instant retail-value payment systems (SPBVI for its Spanish acronym). Based on this mandate, the Bank fostered a public policy agenda aimed at guaranteeing broad access, immediacy, 24/7/365 availability, innovation, efficiency, and security of payments, embodied through the creation of Bre-B.

The design of Bre-B was based on a strategic decision: to build on what had been built, recognizing the existence of multiple SPBVI competing with each other but working in conjunction through centralized components managed by Banco de la República. To this end, the Bank issued a regulatory framework that defines the principles and rules on which the SPBVI must interoperate and determines the technical standards for the processing of immediate operations in an uninterrupted manner.

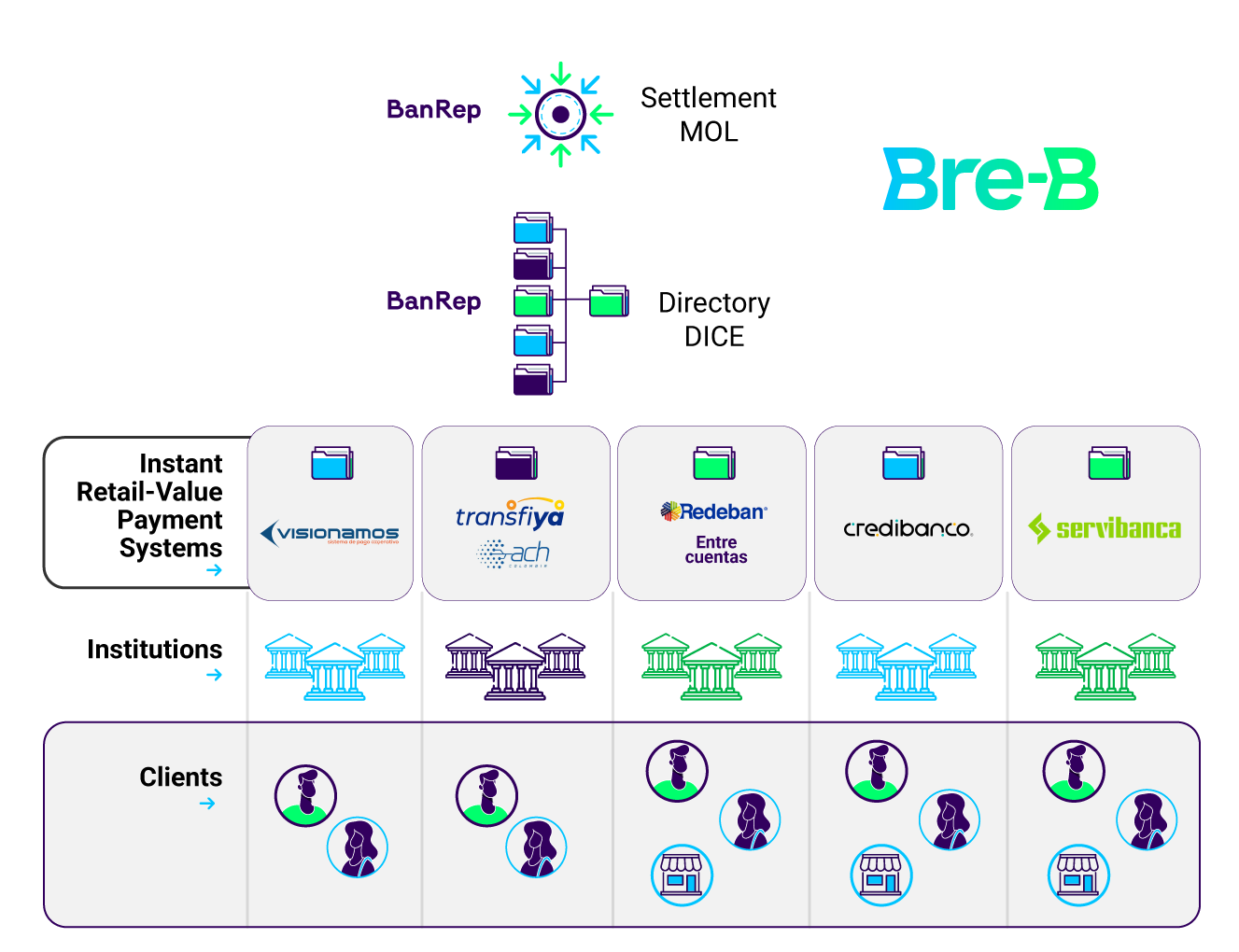

At the beginning of 2023, there was broad coverage of digital wallets, and two working immediate payment services for individuals in Colombia, Transfiyá and Visionamos. In the second half of that year, recognizing expectations about instant interoperated payments, Entrecuentas entered into operation, growing rapidly to become the largest player in the system by 2025. With the launch of Bre-B in October 2025, Credibanco and Servibanca joined this promising sector. The main challenge has been to ensure that all these services communicate with each other, so that any entity in the financial system – as well as other actors authorized to offer payment services – can send and receive immediate payments under a unified mechanism. As of January 2026, Bre-B had 218 participating entities and five fully interoperating SPBVIs, with at least one new entrant (Gou Payments) expected soon.

Regulation was designed in keeping with international standards and constructed with broad participation of the sector’s actors. This regulation established public-private governance through the Immediate Payments Interoperability Committee (CIPI, its Spanish acronym), which serves as an advisory body to Banco de la República, as well as a new architecture in which the SPBVI are interconnected through a digital public infrastructure operated by BanRep. This infrastructure comprises a Centralized Directory of Aliasses (DICE for its acronym in Spanish) and a Operational Settlement Mechanism (MOL for its acronym in Spanish), resulting in Bre-B (Graph 1). The DICE identifies the individual accounts for each customer to receive payments, while the settlement mechanism enables the transfer of resources between the originator and the recipient entity. This architecture allowed the safeguarding of private investments and guaranteed homogeneous conditions for access, security, and operation.

Bre-B’s impact and future strategy

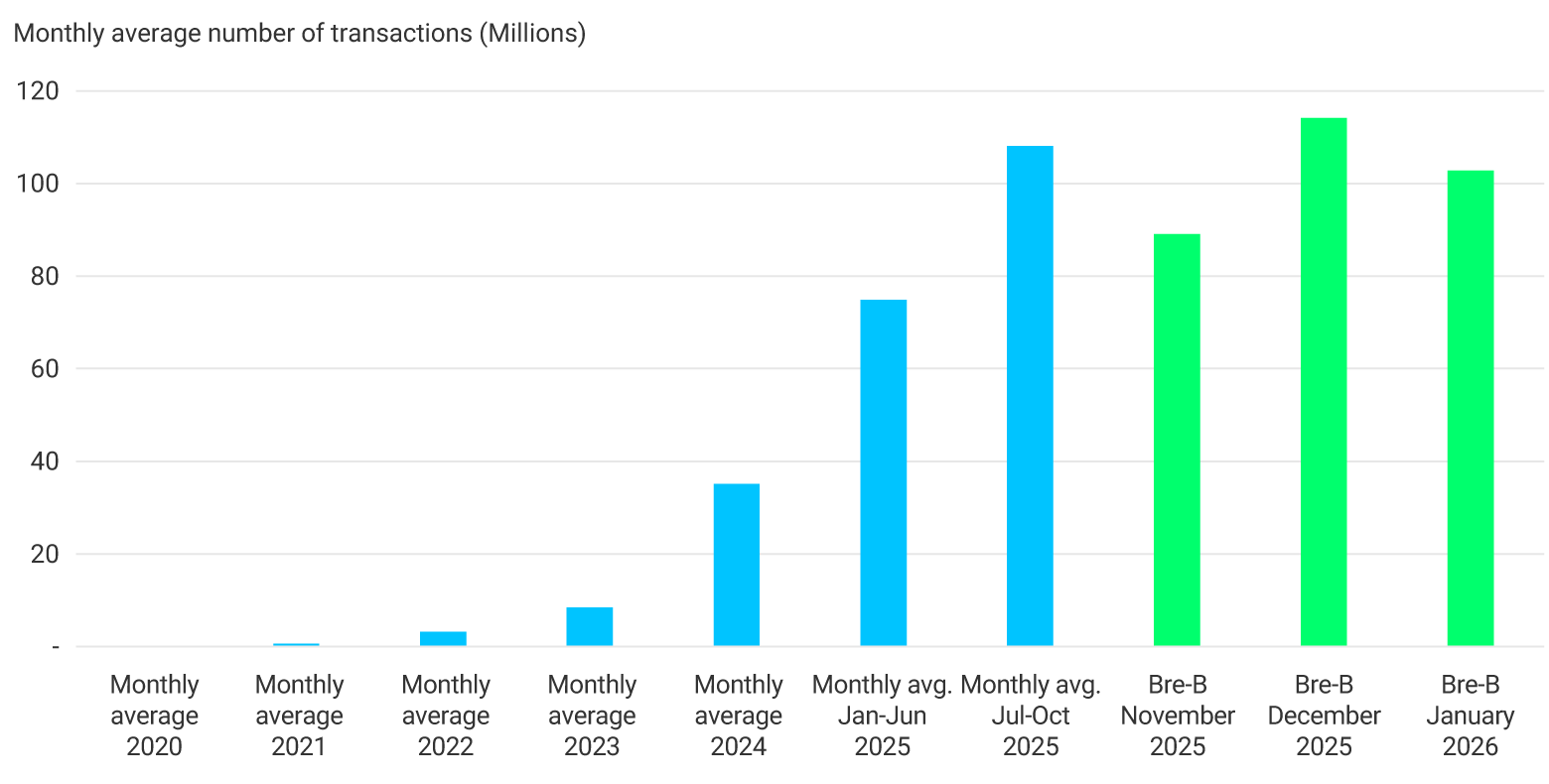

Bre-B became fully operational on October 6, 2025, but its impact had been felt long before. In previous years, the industry conducted pilot projects with unified identifiers under Bre-B’s regulation, QR codes migrated to interoperable standards, and friction and fees across different services were reduced. As a result, immediate transfers grew rapidly even before settlements using the new infrastructure formally began.

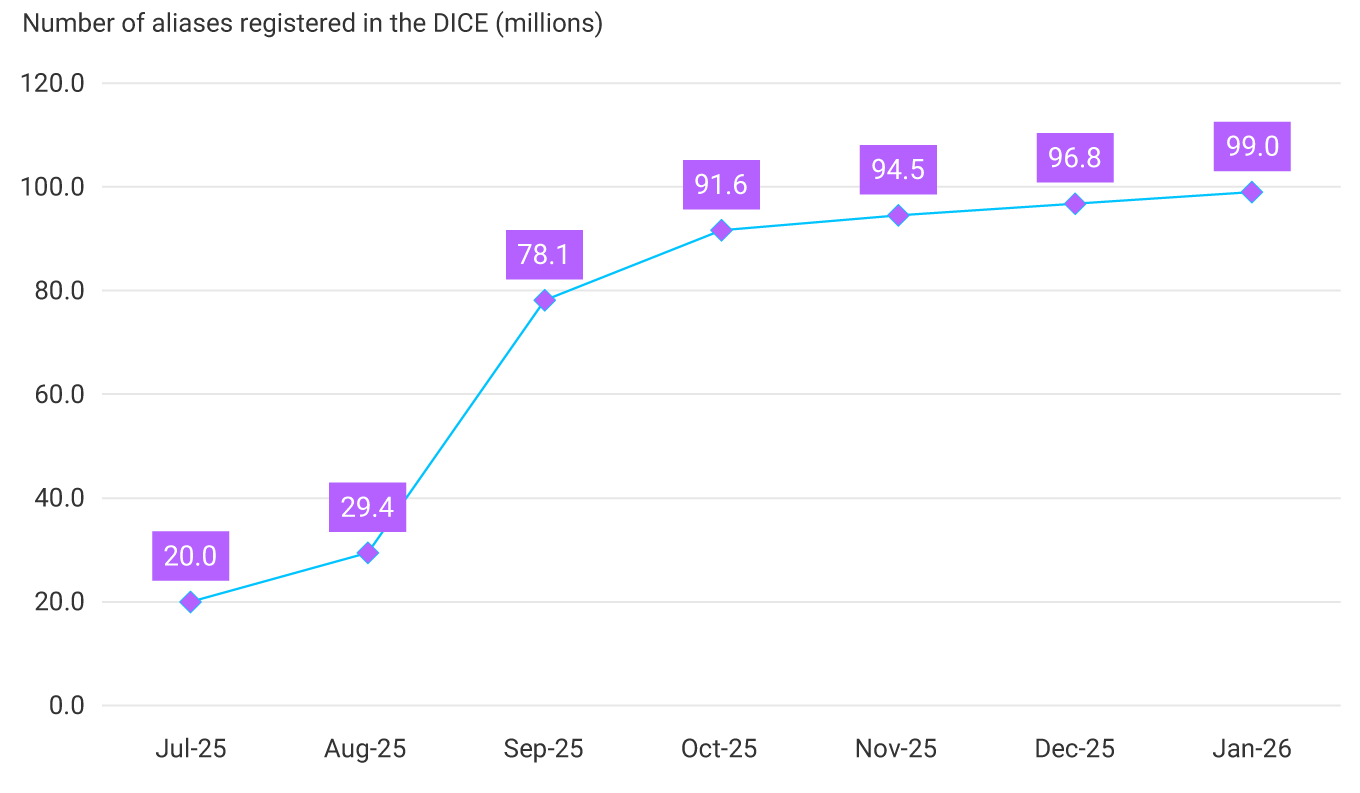

When Bre-B went live, the ecosystem already had a strong user base and activity level. The gradual transition allowed a massive registration of users in the centralized directory (99 million aliases corresponding to more than 33 million customers and 2.8 million merchants) (Graph 2). For their part, most of the transactions previously processed in private systems were settled through the MOL, consolidating the trends observed in previous years by the beginning of 2026, now under a fully interoperated system (Graph 3). In less than four months, until the end of January 2026, more than 370 million transactions were carried out through the operational settlement mechanism, totaling more than 59 trillion pesos.2

Banco de la República has entered a new phase, focusing on strengthening Bre-B, increasing its usage, and broadening its scope. The focus is on providing a unified, simple user experience and building trust through effective fraud-prevention measures and educational initiatives. Additionally, the goal is to enable new use scenarios—including business payments, collections, and e-commerce—and support the entry of new participants.

As Bre-B consolidates around common rules and transactions settle with central bank money, it will continue to foster innovation, competition, and trust, delivering concrete benefits to households and businesses.

1 ↑ Banco de la República (2024). Report on Financial Infrastructure and Payment Instruments 2024.

2 ↑ To learn more about Bre-B and access statistics about its operations with a one-day lag, visit Bre-B (inmediate payments)

3 ↑ Between October 6 and October 31, 2025, a total of 64.4 million transactions were settled through Bre-B.