Monetary Policy Report - October 2024

The Monetary Policy Report presents the Bank's technical staff's analysis of the economy and the inflationary situation and its medium and long-term outlook. Based on it, it makes a recommendation to the Board of Directors on the monetary policy stance. This report is published on the second business day following the Board of Directors' meetings in January, April, July, and October.

Inflation continues to decline, although it is still above the 3% target. Monetary policy measures and correcting factors that pushed prices up are helping inflation to continue approaching the target. Economic activity is recovering to a sustainable level, unemployment has decreased, and the external deficit continues to reduce. The monetary policy interest rate is compatible with inflation being close to the target by the end of 2025 and with the gradual recovery of economic growth.

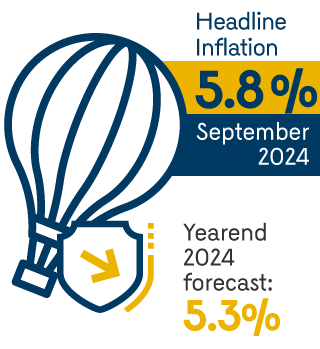

In the third quarter, headline inflation continued to decrease and is expected to continue doing so gradually to reach 3.0% by the end of 2025.

- In September, headline inflation decreased more than expected, standing at 5.8%, and it is projected to be 5.3% by the end of 2024.

- The decrease in the inflation projection is mainly due to the improvement in the supply of processed foods, lower adjustments in electricity and fuel prices, and declining international costs that favored the behavior of some goods prices.

- Service prices, particularly rents and food away from home, showed a slower pace of deceleration due, in part, to the effect of indexation.

- Inflation expectations show a downward trend over time, reinforcing a decreasing dynamic of inflation towards the target by the end of 2025.

- The expected decrease in inflation would continue to reflect the accumulated effects of monetary policy decisions and the correction of factors that pushed prices up in the past.

- The forecasts continue to face high uncertainty related to exchange rate variations, which are at the same time conditioned by volatility in international financial conditions and the challenges of fiscal adjustment in Colombia.

- Other relevant uncertainty factors are the pace of deceleration in the prices of some services such as rents, the behavior of food prices and some regulated goods and services, and the increase in the minimum wage for next year.

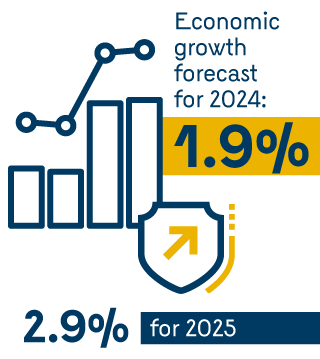

Economic activity continues to show a recovery path compatible with the convergence of inflation to the 3% target. In 2024 and 2025, the Colombian economy is expected to grow by 1.9% and 2.9%, respectively.

- The Colombian economy has been gaining momentum throughout the year, a trend that is expected to continue over the course of the year.

- This recovery is mainly due to higher household consumption, supported by less restrictive monetary policy, better disposable income, and lower financial burden. A greater contribution from public civil works also explains the recovery.

- By 2025, the economy is expected to continue strengthening and reach a level close to its productive capacity, a behavior compatible with the convergence of inflation to the 3% target.

- This behavior would occur in the context of less restrictive domestic and foreign monetary policy.

- The unemployment rate remains low compared to the past, while employment has increased.

- Economic recovery and labor market resilience suggest that monetary policy decisions have contributed to sustainable growth and a reduction in inflation.

- Volatility in international financial conditions and the challenges of fiscal adjustment in Colombia are uncertainty factors for economic activity performance.

The downward trend in inflation and its expectations has allowed the continued lowering of the monetary policy interest rate, which now stands at 9.75%.

- At its October meeting, the Board of Directors of the Banco de la República decided, by majority, to reduce the monetary policy interest rate by 50 basis points (bp), accumulating a reduction of 350 bp since December 2023.

- However, inflation and some of its expectations remain above the target, indicating the need to maintain a still contractionary monetary policy stance to bring inflation to its 3% target.

- Monetary policy decisions continue to support the sustainable recovery of economic growth and maintain the necessary prudence in light of persistent risks regarding inflation behavior.

Monetary Policy Presentation (Only in Spanish)

Box Index

![]() Box 1 - The recent behavior of the rent CPI in Colombia

Box 1 - The recent behavior of the rent CPI in Colombia

Cárdenas, Julián; Rodríguez, Nicol

![]() Box 2 - Infation expectations and their degree of anchoring: what can be inferred from expectations obtained from Colombia’s public debt market?

Box 2 - Infation expectations and their degree of anchoring: what can be inferred from expectations obtained from Colombia’s public debt market?

Muñoz-Martínez, Jonathan Alexander; Parra, Daniel

![]() Box 3 - Recent behavior of foreign remittance infows to Colombia

Box 3 - Recent behavior of foreign remittance infows to Colombia

Sandoval-Herrera, Diego; Hernández-Peñaloza, Mateo