Monetary Policy Report - April 2025

The Monetary Policy Report presents the Bank's technical staff's analysis of the economy and the inflationary situation and its medium and long-term outlook. Based on it, it makes a recommendation to the Board of Directors on the monetary policy stance. This report is published on the second business day following the Board of Directors' meetings in January, April, July, and October.

Inflation continued to decline but remains above the 3% target. Economic activity is gradually recovering, with strong momentum observed in the first quarter of the year. The current benchmark rate remains consistent with inflation’s convergence to the target over the next two years and a gradual recovery of economic growth. However, recent international developments have significantly increased uncertainty regarding the future path of inflation and economic activity.

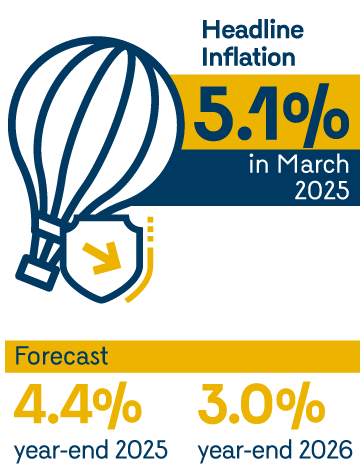

In March, inflation decreased - although less than anticipated - and remains above the 3% target. Over the next two years, it is expected that inflation will continue to decline, converging gradually toward the target.

- In March, annual headline inflation stood at 5.1% - slightly above the forecast - due to upward surprises in regulated items such as gas and urban transportation, as well as increases in processed foods.

- The decline in inflation is largely attributed to the cumulative effects of a still-restrictive monetary policy stance, indexation to lower inflation rates, and the moderation of international prices for certain goods and raw materials. However, inflation remains above 3% due to continued significant price adjustments across all baskets, except for the goods group excluding food and regulated items.

- Core inflation, which excludes more volatile items such as food and regulated items, continued to decline, falling slightly more than presumed to 4.8% in March.

- For the remainder of 2025 and into 2026, headline inflation is expected to continue its downward trend amid a recovery in economic activity, albeit with excess productive capacity, price indexation to lower inflation rates, and moderate exchange rate pressures. Under these conditions, inflation is projected to converge to the 3% target by yearend 2026.

- The inflation forecast remains subject to high uncertainty, particularly due to the behavior of prices for some regulated services and exchange rate dynamics in a context of significant fiscal challenges. This uncertainty has recently increased due to potential impacts stemming from changes in U.S. trade policy.

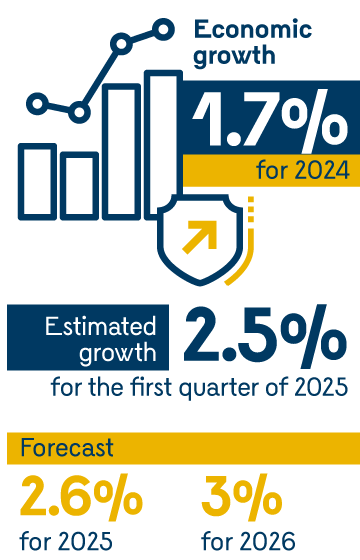

In the first quarter of 2025, economic activity would have recovered more than expected; however, it faces future adverse shocks originating from the external environment.

- In 2024, the Colombian economy grew by 1.7%, broadly in line with projections. This performance occurred against a backdrop of declining interest rates, lower (though still above-target) inflation, and increased household disposable income.

- Available information for the first quarter of 2025 indicates stronger-than-expected economic activity, driven by higher growth in private consumption and investment. As a result, GDP is estimated to have grown by 2.5% year-on-year during the quarter.

- For the remainder of the year, it is anticipated that higher incomes from higher prices of certain agricultural products such as coffee, robust remittance inflows, and strong foreign tourism will bolster economic activity. The latter would be complemented by a gradual recovery in credit amid declining real interest rates and credit risks.

- However, recent tariff increases in the United States and uncertainty about future trade policy have dampened global economic activity, raised global risk perceptions, and increased the cost of external financing, factors that are expected to negatively affect Colombia’s exports of goods and services.

- Considering the stronger-than-expected growth in the first quarter and the adverse external shock linked to global trade developments, the economic growth forecast for 2025 remains at 2.6%, while the projection for 2026 has been revised downward to 3.0%.

- The unemployment rate continues to decline and remains at low levels, while employment has increased significantly, particularly in the non-salaried segment, leading to a rise in the informality rate.

The Board of Directors of Banco de la República (JDBR) continues to adopt a cautious approach to monetary policy, consistent with the aim of guiding inflation toward the 3% target and supporting a sustainable recovery in economic activity.

- At its March meeting, the Board of Directors of Banco de la República (JDBR) opted to lower the monetary policy interest rate to 9.25%, following a decision to keep it unchanged in January.

- Although inflation has declined, it remains above the target and is subject to significant risks, warranting a cautious approach to interest rate decisions to ensure a sustained convergence of inflation toward the 3% target.

- Domestic fiscal challenges and external uncertainty pose significant upside risks to Colombia’s external financing costs, exchange rate, and inflation. These factors underscore the need for a prudent monetary policy stance to support the path of inflation to the target and the sustainable recovery of economic activity.

Monetary Policy Presentation (only in Spanish)

Presentation of the Monetary Policy Report by Hernando Vargas, Deputy Technical Governor of Banco de la República.

Box Index

![]() Box 1 - From recovery to adjustment: recent dynamics of Colombia’s productive sectors

Box 1 - From recovery to adjustment: recent dynamics of Colombia’s productive sectors

Barbosa-Buitrago, Johanna; Pulido-Mahecha, Karen L.

![]() Box 2 - Assessment of the macroeconomic forecast error for 2024

Box 2 - Assessment of the macroeconomic forecast error for 2024

Muñoz-Martínez, Jonathan Alexander; Pérez-Amaya, Julián Mauricio